This Week in CPG 07/27/2026

News from Amara, Terry Ho’s Yum Yum Sauce, A-Sha Foods, Maruchan, Tierra Negra, Halfday Iced Tea, DIME, The Cumin Club, Astadaily, UPDATE, and Soom Foods.

Originally published on LinkedIn Sep 24, 2020

This post has been updated to reflect a dedication to legendary founder Greg Steltenpohl who sadly departed our world this year. Some might remember Adina, his breakthrough brand which is mentioned in this article. He inspired so many and set the beacon for a whole industry.

If we are going to discuss growth, we also must discuss failure.

No marketing or startup team sets out to build an emerging CPG brand that will fail. No CEO starts off with muted expectations and aspirations. Yet, many emerging CPG brands never get to fulfill their very ambitious goals. They wither and die on the vine. They fail.

In 2012, Bevnet [1] estimated that about 300 new beverage brands were entering the U.S. market each year, and that the failure rate was at about 90%. Coke’s Venturing & Emerging Brands Team, a year later, stated that only 3% of all beverage brands reach a $10 million revenue “proof of concept” phase [2].

Dr. James Richardson cites 2017 research in his book [3] that “suggests that roughly 80 percent of premium food/beverage brands fail to make it past $1 million” in retail sales.

The late Harvard Business School professor Clayton Christensen, introduced and contextualized, the often misused, word of Disruption, which has now become part of our day-to-day business dialogue. Christensen is cited in a 2011 Harvard article [4] stating that about 30,000 new consumer products (likely CPG and other consumer products) are launched each year, of which 95% fail!

In a 2019 Nielsen report on innovation [5], Nielsen also reports that 30,000 new products are launched each year. The report notes how this is about the same number of SKUs that is carried by a typical US grocery store. Nielsen further highlighted that, of the products launched, only 30% (9,000) achieve success over the first two years. This breaks down to 20% (6,000) that manage to increase sales and 10% (2,000) that sustained their sales.

Within CPG, there seems to be some confusion with regards to the often-quoted failure rates of 90-95% vs 25-30%. Research by Inez Blackburn, retail expert and Adjunct Professor of Marketing at the University of Toronto, might offer an answer. At the U Connect 08 conference, Blackburn presented research [6] indicating that the failure rate for new product introduction in the U.S. retail grocery industry was 70-80% percent. What is interesting was not the overall number, but rather that while the top 20 US food companies had shown a 24% failure rate, the bottom 20,000 companies had shown a failure rate of 88%. A key difference, Blackburn said, was the “apparent lack of research and strategic marketing done by the bottom 20,000.”

These statistics, some which are now dated but that are likely still within that same ballpark, had always resonated with me given my seed investment and advisory work with technology startups at that time. It resonated because I had come across some in-depth research [7] which had concluded that 90% of tech startups fail to build scalable business models. The two core reasons uncovered, were:

74% of high-growth internet startups failed due to premature scaling. Of these startups that scaled prematurely, 93% were never able break the $100k revenue per month threshold [7].

The tech analog for the CPG category was clear. Premature scaling could be equated to the vast amounts of scarce resources expended by emerging CPG brands to grow distribution too quickly. The problem is not growing distribution per se. It’s the blinding ambition to do that in a manner that, ultimately, does not profitably support that expansion. What I have experienced is that the lack of sufficient trade marketing dollars to support a brand in regions, where that brand is not known, is a large contributor of premature scaling.74% of high-growth internet startups failed due to premature scaling. Of these startups that scaled prematurely, 93% were never able break the $100k revenue per month threshold [7].

Poor product-market-fit equated to the lack of brand resonance or product performance with consumers. This always manifested itself in weak sell-through velocities. In fact, Nielsen’s BASES research [5], found that CPG innovations that launched when they were not ready had shown an 80% failure rate in market. Importantly, the same research highlighted that innovations “with strong product performance were 15x more likely to succeed over the long term than those with poor performance”.

Unfortunately, for a short while, overall sales growth via rampant and undisciplined distribution expansion will mask velocity declines. This happens more often than you think.

The craft beer category is full of lessons of local craft brands that, during the craft beer boom, expanded geographies too quickly. This was achieved at huge expense, only to have to pull out of those same markets many months later. Proliferation occurred quickly, on the back of shelve space expansion. Craft beer was the new gold rush again. As it occurs quite often in certain categories, it did not end well for all. Proliferation eventually resulted in poor and declining velocities. Many liquor stores and grocery stores are still stuck with beers, that have turned “skunky” due to expiration dates that had been surpassed. Several craft breweries are now shutting down. COVID has accelerated these closures, as tap room and on-premise sales quickly vaporized.

Are we going to see the same proliferation risk with Hard Seltzers? My view is a resounding yes. This is a risk for most of the long tail of aspiring brands that are entering the market each week.

It is important to note that not all market pullbacks are a result of poor velocities. In 2011, Dogfish Head (now part of Boston Beer Company) who were growing solidly at the time, wisely retreated from four states. They did this to concentrate their marketing dollars and to guarantee full shelves in markets that that they could support.

It is important to note that not all market pullbacks are a result of poor velocities. In 2011, Dogfish Head (now part of Boston Beer Company) who were growing solidly at the time, wisely retreated from four states. They did this to concentrate their marketing dollars and to guarantee full shelves in markets that that they could support.

The topic of first-mover advantage always conjures up opposing views of whether it is the innovators or the fast followers who eventually achieve the higher levels of success. There are shining examples for both, but if there are lessons to be learnt, let’s highlight two pioneering brands that innovated but that ultimately failed.

Remember Adina? An emerging brand that was way ahead of its time from the legendary Odwalla founder and now iconic and fast-growing Califia Farms founder, Greg Steltenpohl (Bevnet [8] reported the following in 2012:

“The brand has gained distribution through Dr Pepper Snapple bottlers in a few regions of the country, but a nationwide DSD blitz two years ago had failed to create the hoped-for repeat sales that could have elevated the product. While the brand has gradually reduced its price and worked to add zero-calorie SKUs, the future of the Adina “monkey” looked unsure as of today.”

Adina was founded in 2004 and eventually shut down in 2012. They struggled to raise further funding to continue operations. Scaling burns cash quickly and is difficult.

CJ Rapp is the founder and CEO of Karma Water, a functional water with a proprietary cap that dispenses the active ingredients . Rapp recently discussed [9] successes and failures as a beverage entrepreneur and marketer with Taste Radio editor and master interviewer Ray Latif. Rapp, who was known (infamously sometimes) for capturing college students’ gestalt and their need for “staying awake”, launched Jolt Cola in 1985.

The beverage with “all the sugar and twice the caffeine”, was the precursor to the Energy Category as we know it today.

An overnight success and “meteoric” rise in the first year, sales plummeted by 44% in their second year, according to an article [10] in the Rochester Business Journal.

Latif, in a Sep 2020 podcast interview, referred to a comment Rapp made in 2001 when interviewed for a Forbes article [11]:

“If there’s a lesson to be learned, it’s that a good idea by itself is not the single determinant to success.”

Using “brute force” and expensive customer/consumer acquisition discounts to place brands and SKUs on the shelves everywhere is meaningless if consumers are not increasingly and repetitively pulling them off the shelves. Expanding distribution without growing velocity, at the same time, is like planting seeds everywhere in the dessert.

Over the last 10 years, the shift in consumer preferences for craft and natural products played a large role in driving the change in distribution and velocity dynamics within food retailers.

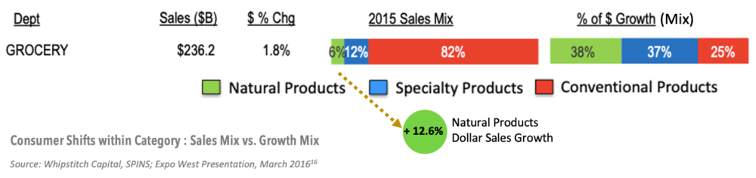

Yet, while on the surface that validated the trend towards more premium and better-for-you options, the reality was that new product introduction was being driven by a higher rate of proliferation. For example, in 2015, according to data [12] from SPINS and Whipstitch Capital, conventional food and beverage products (excl. alcohol) constituted 82% of the sales mix within the grocery departments within the conventional multi-outlet channel, but, captured only 25% of the total growth that year. Specialty and Natural Products made up 18% of the sales mix but had driven 75% of the total growth with grocery departments!

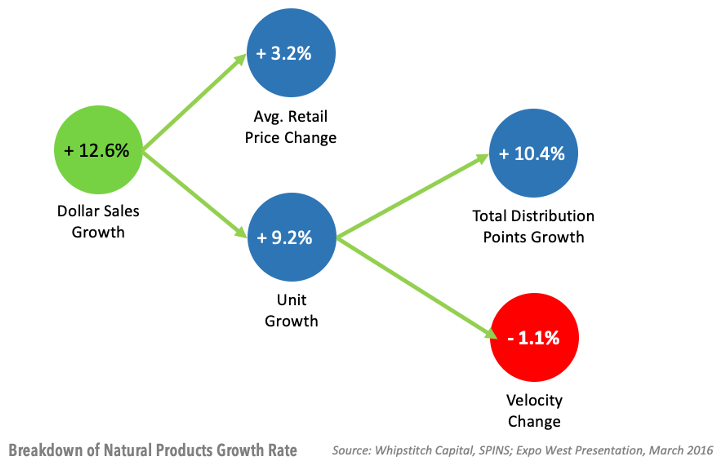

A Nielsen analyses [13] of food/grocery stores between 2013 and 2017, indicated that while distribution points across the Top 5 food categories (dairy, frozen foods, grocery, household care and personal care) had increased, sales velocity had “plummeted”. Contributing factors likely include fewer trips per shopper, the shift to e-commerce, more SKUs/choices, and the ongoing fragmentation between conventional vs natural food products. The velocity warning signals however were there! The SPINS data [12] also showed that the 13 % Dollar growth in natural products, which were replacing conventional products on the shelf, had been driven primarily by a 3% price gain and a 10% gain in Distribution, while velocities had declined by 1%.

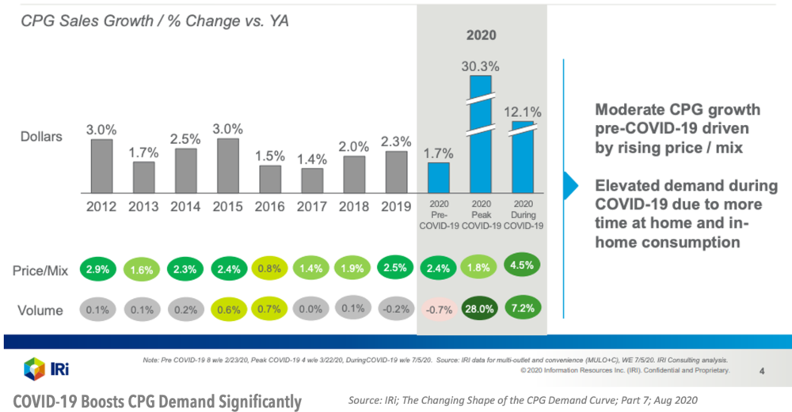

Back to COVID-19. In multi-outlet food retailers, as measured by IRi and Nielsen, year-on year (YoY) growth for many food and beverage categories have remained elevated during this COVID-19 period as compared to 2019 and the pre-COVID period.

IRi reported [14], in early Aug 2020, that CPG demand for many categories were up over 10% YoY versus the “typical 2% to 3% annual industry growth”. At the end of March 2020, CPG YoY sales growth had reached 30%. However, the YoY growth towards the end of July 2020 had moderated to about 12%. Volume growth (pantry loading, increased basket sizes, at-home consumption) had driven the March 2020 peak, while a doubling of price/mix shifts (price increases, trade-up, brand-switching) had contributed significantly to the lift 12% growth experienced in July 2020.

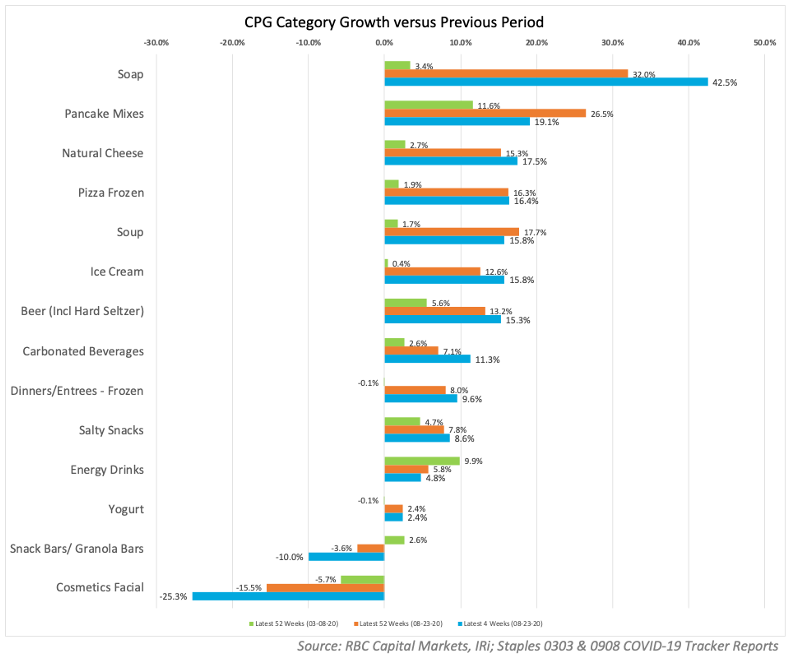

As expected, growth numbers vary at the category level. Nik Modi’s team at RBC Capital has been tracking category growth changes, in conjunction with IRi and Numerator during this COVID-19 period. I have excerpted [15, 16] a few of these categories to show how the various U.S. categories have fared. The charts also show how COVID has impacted at-home consumption behavior shifts. (Note: I did not have data for full 2019 YoY growth rates, so I have used the earliest data set that I had, which would contain a predominant amount of 2019 sales dynamics for those categories)

If you are an emerging brand in one of the sample categories above you might recognize sales growth lifts, or declines, that reflects your reality during the pre and during-COVID periods. For some brands, gains in off-premise retail channels have offset declines in on-premise channels. Craft beers, spirits and carbonated soft drinks are in this group.

For other brands, like those in the snack and granola bar category, the change in snacking-away-from-home has negatively impacted growth. Of course, there are also brands that were always purchased in off-premise channels to “consume at home” and that have completely benefited from the work or stay-at-home shift.

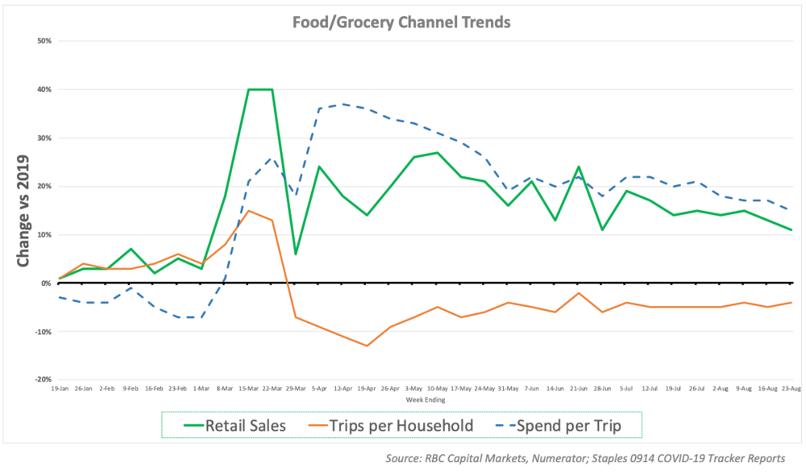

RBC’s analyses also tracked growth across the various CPG channels. I have excerpted the data [17] for the Grocery/Food channel which shows that overall YoY category retail sales growth as of January 2020 was in the 1% to 3% range. The chart below also shows how after the 40% peak in mid-March 2020, retail sales growth indicated an ongoing “decline” to 11% when you look at August 2020. As COVID “fatigue” set in and as the relaxation of shelter-at-home mandates started easing, Spend per Trip also decreased but Trips per Household started inching upwards.

Retailers stocked up. Velocity increased as basket size increased. Core brands and core SKUs flew off the shelf, as retailers doubled-down their efforts and resources to secure supply and placement of those SKUs. Where Out-of-Stocks (OOS) were an issue, retailers scrambled to extend shelf-space to larger brands with more resilient supply chains. However, retailers also reset shelf-space for new or smaller brands that were agile and opportunistic enough to grab that space. As consumers looked for variety in at-home eating occasions, significant trial of emerging brands or less “popular” brands occurred.

This is all good, right? As horrible as the COVID-19 situation is, the truth is that for many brands, COVID came as a boon. Even if a brand had “little chance” of growing at the COVID rates in the pre-COVID era, the swell in that category lifted all the “boats” in that category. There were emerging and incumbent brands, that used this period to strategically recalibrate their portfolio, innovation pipeline or go-to-market approach. These brands knew that:

Needless to say, there are also some previously distressed brands that started celebrating their double-digit growth lifts, without having done anything different from the past. Instead, they myopically accelerated damaging price discounts and simultaneously adopted a scattershot and undisciplined approach to expand in any market or channel. They hit some good numbers, but this delusion of growth will finally catch up to them, and they will be ill-equipped to set a sustainable path moving forward.

COVID or no COVID, the discipline and basic building blocks of building and scaling an emerging brand remain the same. If anything, the Five Growth Imperatives, highlighted above, are even more critical moving forward.

About Manoli

Manoli Kulutbanis is the founder of Biome Botanica, LLC and the Managing Partner of UpScalability, LLC. Manoli recently launched Margin Velocity Planner ™, a decision-support tool that helps founders to build credible velocity-based growth and financial plans for emerging CPG brands. More details are available on marginvelocity.com

References

News from Amara, Terry Ho’s Yum Yum Sauce, A-Sha Foods, Maruchan, Tierra Negra, Halfday Iced Tea, DIME, The Cumin Club, Astadaily, UPDATE, and Soom Foods.

First-time CPG founders often make costly packaging mistakes without realizing it. Discover eight common missteps and how to create packaging that stands out, communicates clearly, and sells more effectively.

Distributor deductions can quietly drain a CPG brand’s margins, especially when there is no clear process for planning, reviewing, and disputing them. In this episode, I sit down with Yuval